Since the Bank of Canada lowered interest rates as “insurance” against the risk of a sharper downturn, many have been asking: How long will it take for the fall in oil prices to impact the broader economy and how severe will the slowdown be? What will it mean for Canadian business?

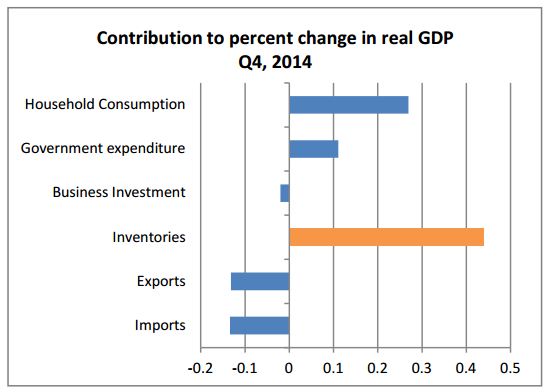

Canada’s fourth-quarter GDP growth came in at a brisk 2.4%, which looks pretty good, but when we examine where the growth came from, there is cause for concern. Household consumption was OK, but exports and business investment both declined. Instead, you can see in the adjacent graph that the biggest contributor, accounting for three quarters of the rise in GDP is inventories.

A sharp rise in inventory can be caused by businesses stocking up in anticipation of stronger sales in the future or, alternatively, if a sharp deterioration in demand leaves unwanted stock. What’s the likelihood that business was stocking up in anticipation of a bonanza at the end of 2014? Not very good. Instead, we’ve heard anecdotally that companies in the oil patch were hit with a particularly sharp drop in sales, and the concerns are broad-based with the auto sector accounting for a big part of rising inventories.

There are three reasons we’re expecting a significant slowdown in Canada. Firstly, the big declines in capital expenditure have not yet been seen in the broader economy. Remember that oil prices remained above $75 until the middle of November and only fell into the $50 range in December. There were many announcements of cutbacks at the end of 2014 but these will not be seen in operations on the ground until the first half of 2015, a point confirmed by many service providers in the energy industry.

Secondly, consumption looks soft as retail sales fell by 1.7% in January, signs that consumers are staying home. Also, that big boost from inventories will reverse and become negative in the quarters ahead as the closures of Target, Mexx, Jacob and Sony subtract billions from the inventory tally this year.

Thirdly, it is true that many manufacturing industries are seeing a boost in sales from the weaker loonie and a stronger U.S. economy. Canada’s auto sector and aerospace industry exports have been particularly stellar. However, oil and gas accounts for 24% of Canadian exports, and those prices have fallen by half. It will take a long time before manufacturing can compensate for a 12% hit to Canadian exports.

Canada’s domestic economy has a hit a soft patch, so we should be braced for bad news in the first half of 2015. Overall GDP growth should come in around 1.8% this year, and Canadian businesses will have to focus more than ever on exports if they want to maintain the strong growth rates we’ve seen. In the meantime, it looks like we may need that insurance.

-Hendrik Brakel, Canadian Chamber of Commerce